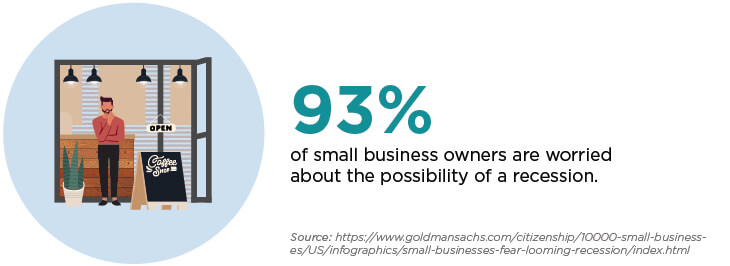

No one knows for certain whether we’ll enter a recession in the next year, but if you’re concerned about your small business, you’re not alone. About 93% of small business owners are worried about the possibility of a recession, according to a June 2022 survey by Goldman Sachs.

Regardless of what the future holds, now is a good time to prepare your business. This nine-part framework will guide you through steps to recession-proof your business. With some preparation, you can meet a potential downturn on your own terms.

We’ll walk through tips across three categories: Your finances, your business relationships, and innovation.

Prioritize Your Finances

The first step in recession-proofing your business is to implement strategies that bolster your bottom line.

1. Focus on cash flow.

Cash flow is the lifeblood of any small business. It can also be a significant source of anxiety. Here are some ways you can take control of your cash flow today.

- Evaluate your expenses. There are often ways to cut back on even the most necessary expenses. Ask yourself:

- Do your vendors have other pricing options that work better for your cash flow?

- Are other vendors offering the same goods or services at a better price?

- Can a lower tier of services meet your needs just as well?

- Can you manage debt more effectively by consolidating your debt load?

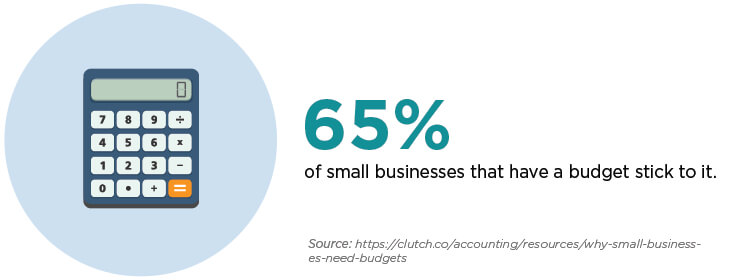

- Give your budget a tune-up. According to a recent survey, 65% of small businesses that have a budget stick to their budget. Try these tips to get more strategic with your budget:

- Account for your time. Time is money, too. For example, you might save money by cutting back your virtual assistant’s hours. But when you factor in the time it takes you to do their tasks, the cutback might actually cost you.

- Check in with your budget regularly. Schedule time to work on your budget. Use check-ins to adapt your budget to your business’s changing needs, whether you’re responding to a seasonal trend or experiencing an unexpected dip in revenue.

- Overestimate your expenses. This gives you some breathing room to counteract unexpected costs that might surface from month to month.

- Tighten your receivables process. Your receivables can have a big impact on your access to funds. Consider streamlining your receivables process by:

- Sending invoices when you finish a project or at specific milestones of completion, rather than sending out all invoices one day a month.

- Monitoring outstanding invoices so you can send reminder notices sooner rather than later.

- Offering early payment discounts to incentivize quicker customer payments.

2. Establish an emergency fund.

An emergency fund offers peace of mind. But cash flow issues often prevent business owners from saving as much as they’d like. So how can you build an emergency fund now, when business is stable?

- Obtain a line of credit. The best time to obtain a low-fee, low-interest line of credit is when your business is doing well. This can also allow you to absorb the low fee without racking up additional debt.

- Collect on late receivables. Late payments are the bane of most business owners. Now could be the time to implement a more assertive collection policy and charge a fee on late payments. This can be a tricky line to walk: You don’t want to lose existing customers by being too aggressive, but at the same time, you deserve to be paid on time.

- Increase your revenue. It may seem easier said than done, but there are some easy ways to increase your revenue, including:

- Renegotiating your contracts with vendors and customers to obtain better terms.

- Offering different pricing options, such as subscriptions, to attract new customers.

- Leveraging the 80/20 rule: Concentrate most of your efforts on nurturing relationships with your best customers.

3. Keep marketing.

Marketing is vital to your small business’s financial success. Here are some ways you can keep up marketing efforts without a big budget:

- Tie your marketing spend to your revenues. Keep your marketing budget flexible by setting it as a percentage of your projected revenue.

- Explore low-cost digital marketing methods. Establishing a strong online presence through your website and social media channels can help keep your business top-of-mind for customers.

- Track your marketing return on investment (ROI). Tracking the return on your marketing spend lets you focus on the marketing efforts that get you the best results.

Invest in Your Relationships

Relationships are important to any small business’s success. In unstable economic times, relationships can become vital to your business’s survival.

4. Nurture your customers.

Your customers are likely as worried about a potential economic downturn as you are. Here’s how to maintain customer relationships so your product or service won’t be a part of their budget cuts:

- Create a customer loyalty program. A customer loyalty program is one way to reward your best customers and keep them coming back. Your program doesn’t have to be extravagant: Minor discounts and points-based rewards can add value in your customers’ eyes.

- Focus on customer service. A 2020 survey found that 94% of customers would be likely to recommend and purchase more from businesses they had a “very good” customer experience with. Consider creating a customer service policy so both you and your employees have guidelines for providing a consistent, quality experience.

- Leverage the power of after-purchase service. Post-purchase customer follow-ups provide a way to connect with customers in an authentic and helpful way. These interactions also allow you to nip dissatisfaction in the bud by addressing problems before they arise.

5. Don’t forget about your employees.

When it comes to running a small business, good employees are invaluable. Of course, if you feel you have too many people on staff, cut-backs may be necessary. But it’s vital to remember that quality customer service is important during economic downturns, and your employees play an important role in maintaining that quality. Here are some tips you can follow:

- Prioritize employee retention. Training and onboarding new employees can be costly. By focusing on your current employees, you can build a loyal team that functions as the backbone of your business.

- Invest in employee cross-training. Building your employees’ skills can go a long way during recessionary times when you may not have funds to hire additional staff to meet unexpected needs.

6. Form strategic alliances.

Forging strategic alliances with vendors, suppliers and businesses that provide complementary goods or services can help stabilize your business during rocky economic times. There are benefits to having a network of allies to lean on:

- It’s easier to make the hard ask. Having a strong relationship with vendors and suppliers establishes trust. That trust is precious if you ever need to make a difficult ask, whether you need a few more days to make a payment or you’re renegotiating for better terms.

- You can expand your marketing reach. Aligning your business with complementary businesses can be a win-win for everyone’s marketing efforts. Something as simple as promoting each other’s discounts could double your business’s reach.

Focus on Innovation

When you think of innovation in business, you might imagine tech startups. But innovation plays a significant role in the success of small businesses, too.

7. Diversify your products and services.

Diversifying your products and services can be an excellent recession-proofing tactic: If the market for one product or service dries up, you’ll still have others to fall back on. Here’s how to start diversifying:

- Broaden your market. Brainstorm ways to expand your target market by offering new lines of products or services. For example, the owner of a miniatures and collectibles hobby store knows that some of their customers use collectibles in games. The owner might consider adding tabletop board games to their inventory and running gaming tournaments on weekends.

- Consider niching down. You don’t always have to broaden your offerings to diversify. Offering new products by niching down can help you cultivate a loyal customer following. For example, if you run a bakery, expanding into specialty goods such as gluten-free or keto-friendly items could attract a dedicated group of new customers.

8. Expand your revenue streams.

By adding additional income streams, your business will be better positioned to absorb a decline in any one area. Here are a few ways to consider expanding into new income streams:

- Create a digital product. If you sell physical products or provide local services, consider branching out into the digital arena. For example, a plumbing store could create and sell a video-based DIY guide to common residential plumbing issues.

- Generate ad income from your digital assets. Websites, blogs and email newsletters can become vehicles for regular monthly income through ad placements and sponsorships. For example, if you send out a weekly email to your clients, try approaching complementary businesses about sponsoring your newsletter.

9. Power up your systems using tech.

Making a small investment in new technology can have a major impact on your bottom line by saving you time or money—or both.

- Automate to save time. According to the Zapier 2021 State of Business Automation report, 34% of small businesses said that automation reduced time spent on admin work. How can automation help save you time? For starters, look to accounting software. Many accounting tools notify you when outstanding invoices are overdue and even send automatic reminder emails to your clients.

- Take advantage of the tech you’re already using. Most business software these days is full of features you may not even know about. For example, some payroll softwares do more than manage payments. Many programs also offer features like tax filing services and regulatory compliance management.

Even with the possibility of a recession on the horizon, you can take steps now to prepare and ensure your small business survives whatever lies ahead.

Next steps: Interested in more small business tips? Sign up for the Small Biz Ahead newsletter today.

And keep learning. My mantra, if you are not earning you better be learning. Skill upgrades, new skills, or even take a vacation. Anything that expands your thinking.

This is a great point, Marcus. Thank you for sharing it!