The discounted cash flow (DCF) approach is a powerful tool that can help you understand the true value of a business or investment. By applying an appropriate discount rate, you can determine whether an investment opportunity offers real potential going forward or poses more risk than reward.

Whatever type of major purchase you’re considering, learning how to calculate discounted cash flow can help you make more informed and confident decisions. In this guide, we’ll explain the key components behind an accurate discounted cash flow statement, walk you through the DCF formula and show you how to estimate what something is worth today based on the estimated cash flows it’s likely to generate in the future.

What Are the Components of DCF Analysis?

- Periods of time.

- The projected cash flow that will occur every year.

- A discount rate or annual rate. The discount rate could be thought of as how much money you’d earn if you invested it in another account with equal risk.

- The terminal value. This number represents the perpetual growth rate for future years outside of the timeframe being used.

The method takes your projected cash flows and discounts them using an annual rate to calculate their net present value (NPV), which can then be used to determine the overall potential for a given investment.

However, before you can accurately forecast these numbers, it’s essential to review your company’s cash flow statement to understand your current inflows and outflows.

What Is the Discounted Cash Flow Formula?

This is the DCF formula:

(Cash flow for the first year / (1+r)1)+(Cash flow for the second year / (1+r)2)+(Cash flow for N year / (1+r)N)+(Cash flow for final year / (1+r)

How Do You Calculate the DCF?

The discounted cash flow calculation can be as simple or complex as you want.

- Cash Flows: These represent the money coming into and going out of the business during each period. For a business, cash flows include revenues, operating costs and capital expenditures. For a bond, cash inflows and equity value are based on interest payments and principal repayment.

- Discount Rate (r): The required return an investor expects is often based on the weighted average cost of capital (the average rate a company pays to finance its assets), which combines the cost of equity and debt financing. A higher rate lowers the calculated value of future earnings and a lower rate increases today’s estimated value.

- Number of Periods (N): Choose a forecast period that matches your investment horizon. It could be 5, 10 or even more years depending on the asset. However, keep in mind that extended timelines require more reliable figures for forecasting future cash flows.

- Terminal Value (TV): This represents the growth rate for future earnings outside of the timeframe you’re using. It’s calculated by taking the final year’s cash flow, adjusting it for growth and dividing it by the difference between your discount rate and growth rate.

Finding the necessary information to complete a DCF analysis can be a lot of work. But when you’re able to plug in the information into the formula, it becomes a simple calculation. There are plenty of discounted cash flow calculators online if you need more help.

Once you get the DCF value from the formula, you can more accurately assess the value of your potential investment. All you need to do is compare the figures. If the DCF value is higher than what you’d pay today, it may signal a strong investment opportunity. If it’s lower, that could be a sign that future performance may not deliver the returns you expect.

Discounted Cash Flow Valuation Formula With Examples

To calculate a company’s intrinsic value using the DCF method, you first estimate future performance, then discount back to today’s value using an appropriate discount rate. Here’s how to do it, along with some examples of how your calculations may pan out in different scenarios.

Step 1: Estimate Future Cash Flows

Look at the company’s financial statements to project annual cash inflows and capital expenditures over a set forecast period. For example, if last year’s cash flow was $25M and you expect 5% annual growth for the first two years, then 2% for the following three, your projections look like this:

| Year | Cash Flow | Calculation |

|---|---|---|

| Year 1 | $26.25M | $25M × 1.05 |

| Year 2 | $27.56M | $26.25M × 1.05 |

| Year 3 | $28.11M | $27.56M × 1.02 |

| Year 4 | $28.67M | $28.11M × 1.02 |

| Year 5 | $29.24M | $28.67M × 1.02 |

Step 2: Calculate Terminal Value (TV)

Once the forecast period ends, calculate the terminal value to capture future earnings beyond Year 5. You do this by using the following formula where g = the long-term growth rate and r = the discount rate.

Terminal Value (TV) = Final Year Cash Flow × (1 + g) ÷ (r − g)

For instance, if the final year’s cash flow is $29.24M, the long-term growth rate (g) is 3%, and the discount rate (r) is 4% the terminal value equals $3,011.72M.

Step 3: Discount Cash Flows To Present Value

Now that you have your projected cash inflows and terminal value, the next step is to discount them back to today’s value using the discount rate. This converts future earnings into what they’re worth right now.

Using the example above and a 4% discount rate, the calculation looks like this:

DCF = (26.25 / 1.04^1) + (27.56 / 1.04^2) + (28.11 / 1.04^3) + (28.67 / 1.04^4) + (29.24 / 1.04^5) + (3011.72 / 1.04^5)

When you add these together, the discounted cash flow value comes to $2,599.66M.

Step 4: Interpret the Results

All you need to do now is compare this figure to the company’s current market-based valuation or stock price and see how it stacks up against competing investments. In our example, the company’s enterprise value is approximately $2.6B when adjusted for discounted cash flow, meaning buying the company for less than that amount would likely deliver returns above the initial cost.

How Do You Calculate DCF in Excel?

If you want to perform a discounted cash flow analysis on the computer with Microsoft Excel, there isn’t a specific formula for it. However, you can set up a spreadsheet to perform the calculations for you.

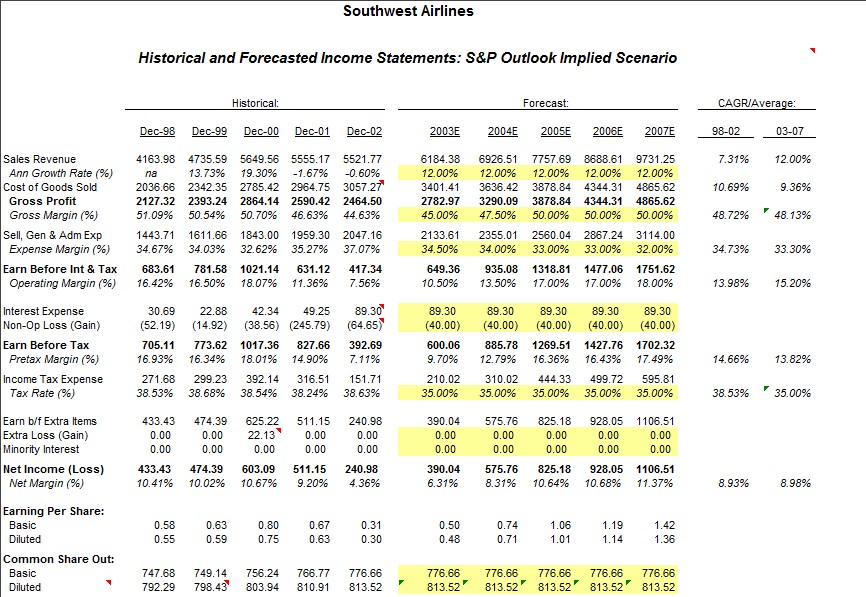

Here’s an example of what an Excel spreadsheet for a discounted cash flow analysis looks like:

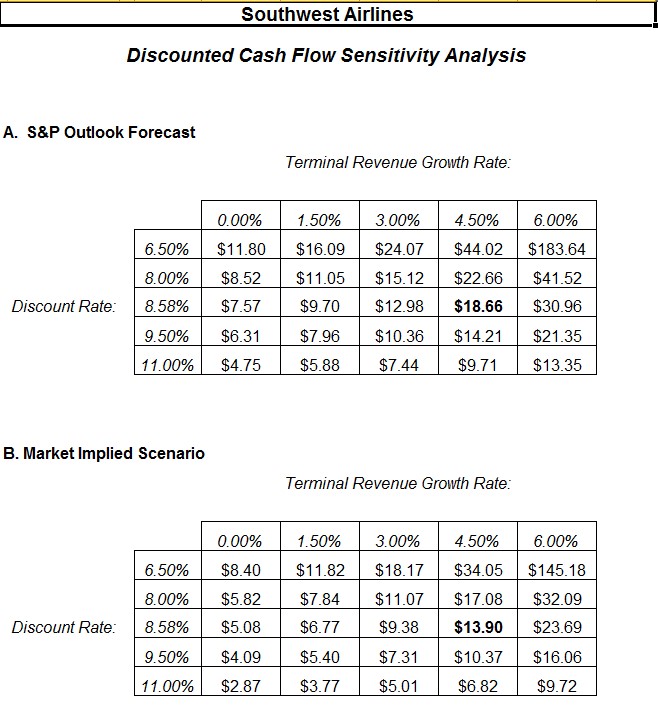

Using Sensitivity Analysis in Excel for DCF

Once you’ve calculated your discounted cash flow, it’s useful to test how changes in your assumptions might affect the final value. This is where sensitivity analysis comes in. By adjusting key inputs — like growth rate, discount rate, appreciation or forecasted cash outflows — you can see how changes in key variables might impact the company’s capital budgeting.

You can set up a simple data table in Excel to compare variables side by side and visualize how much the valuation changes under different conditions. Here is an example.

Uses of DCF Analysis

Discounted cash flow has long been one of the core methods for valuing investments. It is especially useful when inflation, interest rates or market volatility highlight the importance of understanding an asset’s fundamentals. While in very low interest-rate environments DCF outputs can sometimes appear less informative (because discount rates are so close to zero), the method has remained a central valuation tool in corporate finance, investment banking and private equity.

Common applications include:

- Corporate finance valuations: Determine if a company’s stock or equity capital is under or overvalued.

- Mergers and acquisitions: Assess whether buying another company would deliver long-term returns.

- Capital budgeting: Decide whether large purchases, such as equipment or property, are likely to generate sufficient future revenue to justify the initial investment.

- Comparing investments: Weigh competing opportunities to see where your capital is best allocated.

Because DCF relies on projections, it’s most effective when you have reliable data to fuel your estimations. For that reason, newer businesses or those with limited history, may use alternative valuation with capital asset pricing model methodologies to provide better insights.

Discounted Cash Flow Application Tips

Successful utilization of the DFC method hinges on making realistic assumptions. Here are some practical tips for choosing the right period for your analysis, selecting an appropriate discount rate and interpreting your findings.

How To Come up With the Right Time Frame for DCF

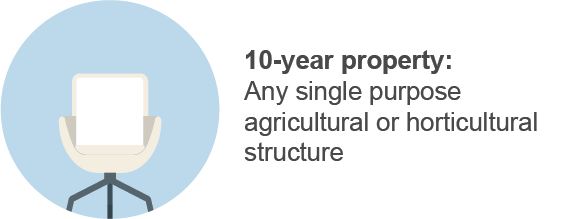

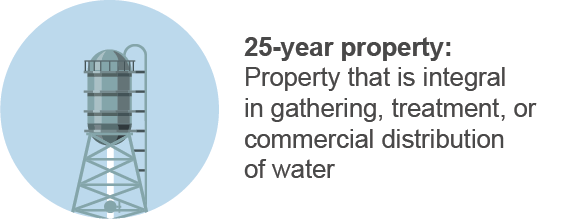

Choosing the right forecast period is critical. The ideal timeframe varies based on the asset or investment you’re valuing. For physical assets, the IRS provides depreciation schedules that can help guide you:

- 7-years: Office furniture, fixtures, agricultural machinery and equipment.

- 10-years: Single-purpose agricultural or horticultural structures.

- 15-years: Land improvements like fences, roads, sidewalks, bridges, municipal wastewater plants and qualified restaurant property.

- 20-years: Farm buildings and municipal sewers.

- 25-years: Property used for gathering, treatment or commercial distribution of water.

While this provides a realistic guideline, you may need to make some adaptions based on the specifics of your investment. The goal is to select a timeframe that’s long enough to generate meaningful figures while ensuring realistic data to support your projections. Try using real numbers wherever possible. Comparing historical figures helps ensure your projections are grounded in reality.

How To Determine the Correct Interest/Discount Rate for DCF

A higher rate lowers the present value of future earnings, while a lower rate increases today’s estimated value. Here are a few tips to guide your decision:

- Use WACC as a baseline: For many businesses, the weighted average cost of capital (WACC) is the standard choice as it factors in the cost of both equity and debt financing.

- Consider current interest rates: If you’re valuing a specific purchase like equipment or property, the discount rate often aligns with typical borrowing rates for similar investments.

- Account for inflation: Since expected future cash flows lose purchasing power over time, your discount rate should reflect inflation trends.

- Be realistic: Accuracy matters. Overly aggressive assumptions can distort your valuation, so conservative inputs are essential for reliable results.

Even small changes can significantly impact your overall valuation and estimations of free cash flow in the future, so always choose a rate that reflects both the risk of the investment and the return you would reasonably expect.

Weighing the Advantages and Disadvantages of the Discounted Cash Flow Methodology

The discounted cash flow method is a powerful way to estimate the potential value of an investment. However, like any other valuation approach, it has its strengths and limitations.

Advantages of DCF

When applied correctly, the DCF method can give you valuable insights into an investment’s true worth. Here’s a list of key benefits:

- Focuses on fundamentals: Uses projected cash inflows and outflows rather than relying solely on market prices or comparable company analysis.

- Captures intrinsic value: Helps determine what an investment is truly worth today based on future earning potential.

- Flexible for different scenarios: Can be adjusted to test investment opportunities under varying conditions.

- Useful across contexts: Widely applied in corporate finance, mergers and acquisitions, capital budgeting and evaluating competing investments.

DCF’s strength in measuring value based on long-term fundamentals makes it a go-to tool for accurate and realistic evaluations.

Disadvantages of DCF

Of course, no valuation tool is perfect. Here’s a quick list of the primary drawbacks:

- Highly sensitive to assumptions: Small changes in variables can significantly alter the results.

- Requires accurate projections: Overly optimistic or unreliable estimates can distort valuations and lead to poor investment decisions.

- Terminal value dominates: In many cases, more than half of a company’s DCF value comes from the terminal value, making the model vulnerable if long-term growth assumptions are off.

- Time-consuming and data-heavy: Gathering reliable inputs, performing calculations, and testing scenarios can be complex, especially for companies without a long financial history.

The bottom line is that accuracy depends on having reliable data and realistic assumptions. Knowing which mistakes to avoid when calculating a DCF is helpful. But even still, it’s generally considered best practice to cross-check with other valuation methods for a more

Discounted Cash Flow: Helping Determine the Value of an Asset

If you need to know if it’s worth the investment to buy a business, piece of equipment or any other asset, the discounted cash flow can help.

By adding up the projected cash flows within a certain time period and discounting the money to the net present value, the DCF analysis can show you how much money you’ll get in return from your investment.

FAQ About Discounted Cash Flows

Why is it called a discounted cash flow?

It’s called a discounted cash flow because the model estimates the value of future cash flows after “discounting” them back to their value today. This reflects the fundamental principle behind DCF — that money today is worth more than the same amount in the future.

Is discounted cash flow the same as IRR?

No, the discounted cash flow method is a financial analysis tool that calculates the present value of projected cash flows, while the internal rate of return (IRR) is the discount rate at which those cash flows break even (i.e. when the net present value equals zero).

Is DCF the same as NPV?

No, DCF is the process used to calculate the net present value (NPV) of projected cash flows. NPV is the actual dollar amount you get after discounting future cash flows back to today’s value.

What is the biggest drawback of the DCF?

The biggest drawback of the DCF model is its sensitivity to assumptions. It’s all too easy to look at an asset and overestimate how much money it will make in the future, leading to a higher result and an inaccurate valuation.

Great Article! Thanks a lot.

You’re welcome! We’re glad you liked it!

Great article! It was articulated superbly and helped me get past some roadblocks I ran into from class.

We’re so glad it was helpful, Andre!

Thank you for the piece of valued information