As a business owner, you need to be prepared to handle any setback. This includes natural disasters. So, how do you ensure the survival of your small business after such a devastating event?

In episode #92, Elizabeth Larkin, Gene Marks and their special guest, CEO Paul Quintero of Accion, discuss not only how you can prepare your business for natural disasters, but also how to diminish its recovery time once they actually occur.

Executive Summary

1:09—Today’s Topic: How Do I Ensure the Survival of My Business During a Natural Disaster?

5:14—The first response to any natural disaster is to keep your business running or reach out to financial resources that will enable you to stay open.

6:03—Make sure that the needs of your employees and clientele are taken care; your business cannot fully recover until those who contribute to it have access to adequate shelter and other basic necessities.

8:58—Take into account the time it takes actually access the necessary relief funds and plan accordingly.

10:50—Business owners should familiarize themselves with all quick-funding resources and economic first responders prior to any disasters, so that they can diminish the time it takes to receive the necessary help.

17:24—Prepare your business for the unexpected by building your own financial reserve and establishing a line of credit beforehand.

19:03—Invest in some form of insurance as well as any devices that can physically enable you to keep your business running during a disaster.

Links

Download Our Free eBooks

- Ultimate Guide to Business Credit Cards: The Small Business Owner’s Handbook

- How to Keep Customers Coming Back for More—Customer Retention Strategies

- How to Safeguard Your Small Business From Data Breaches

- 21 Days to Be a More Productive Small Business Owner

- Opportunity Knocks: How to Find—and Pursue—a Business Idea That’s Right for You

- 99 New Small Business Ideas

Submit Your Question

Transcript

Elizabeth: Welcome back to another addition of the Small Biz Ahead Podcast. Today, we have a special guest and we’re going to be talking about a special topic that’s been in the news a lot lately. Our special guest today is Paul Quintero, he is the CEO of Accion headquartered in New York. Paul, tell us a little bit about what Accion does, and then we’re going to introduce our topic for the day.

Paul: Accion is a non-profit loan fund created to provide access to capital and this is support for business owners that can’t access funds from traditional sources. For a little over 25 years, I like to say we help fulfill big entrepreneurial dreams through small loans, and particularly early stage businesses, credit-challenged businesses, the plurality of business owners out there today.

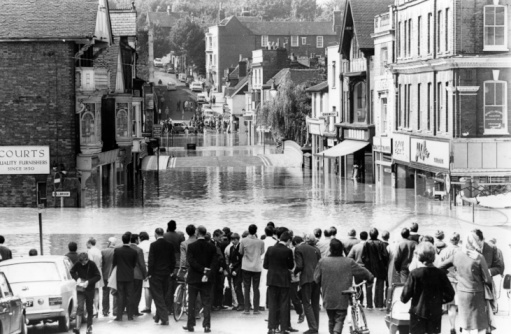

Elizabeth: Okay, great. What we’re going to be talking about today is disaster recovery. Gene, this is something that we’ve seen in the news a lot, unfortunately, this past year. We’ve had several major storms, we’ve seen some small business owners lose their businesses, unfortunately, have their property severely damaged. We’ve also seen some business owners rise to the occasion and get a lot of great PR about how they’ve reacted to the storm, and how much they’ve gone out of their way to help their communities.

Gene: Paul, it’s really great to speak with you. Before we even get into the whole surviving a disaster and all of that, I’m a huge fan of Accion and you guys, just to make sure I also understand, one of the real sort of unique things that your company does is you really hand-hold businesses through getting a loan. I met one of your customers just a few months ago that was looking to expand his … He had a food truck, and he was going to expand his business into an actually restaurant restaurant. He was working with you guys, you guys were not only, not only helped him with financing but actually helped him to find tables and chairs and equipment and get good deals on things that he needed to spend his money in the right way. That’s the kind of stuff that you guys do, right?

Paul: That’s exactly right. The mission, our mission statement, talks about Accion and capital, but people always forget business support. We try to remind people that money doesn’t console, comfort, or advice. People do. People are the heart of what we do, and that direct one on one relationship is key. I think the other part that you were kind of alluding to is that what makes us different as a mission oriented organization is that we’re not in this for a transaction. We’re in this for the transformation. We succeed if the business owners succeed, and I think that’s a really big differentiator from what people might otherwise find in more transactionally-oriented, profit-maximizing kind of organization.

Which, should exist and they have a good service, but we’re really there to see that change happen.

Gene: That make sense. You guys are a non-profit, so again, people can go to a bank for a loan or a traditional sources. Whether they can get it or not, that’s another matter, but coming back to you, that’s just an extra value added. Relationship that you bring in to not only helping with financing, but also helping to use financing the right way.

Paul: That’s right. Connecting people to resources is a big part of what we do. The social capital that a business owner needs is as critical as the financial capital.

Gene: Makes sense. That kind of dovetails into the actual main topic of this conversation today, which is about natural disasters, and businesses recovering from disasters. I have a bunch of questions to ask you about that, and what business owners need to know. I had just written recently about Houston, which obviously just went through a terrible hurricane, and flooding. So many businesses were affected and so many people were affected, and now they’re recovering. Now I’m reading there was a recent survey that came out by a national bank that said that business owners in Houston, this survey was taken after the storm, are optimistic about next year because … Clearly with all the bad things that happen in a disaster, once people get sorted out and back on track, there’s a lot of opportunity for businesses.

What kind of experiences have you had with businesses that have gone through or experienced the major storm? With their recovery process, is it quick? Does it take a long time? Do you have any thoughts or stories to share?

Paul: Absolutely. You know, it really does depend on the impact or damage created by a particular disaster. I think the only thing that’s universal is that it can be potentially dangerous, but how it actually manifests, and every region can vary. Our first, I guess it depends, let’s talk about natural disasters. In 2012, in the New York area, we had Hurricane Sandy. This year, as you said, we had Harvey. Irma, which I’ll talk about a little bit more because it directly affected not only the clients we serve, but even our own staff offices in Florida. Of course, Maria, that pretty much devastated Puerto Rico. What we know, from these experiences, is the role that we can play at Accion is to be an economic first responder. What that means is in the first 90 days from when a storm, and I mean something that knocks out activities.

You have storms, and they can do some damage to property, but when we get to a point where we have critical services or infrastructure that get affected, or even paused, that’s when damage starts to kick in. We know that in the first 90 days, if we’re able to go in and help someone stave off essentially shutting down, that’s the best help that we can provide in the interim. Once you do shut down, the statistics show in these storms very few businesses come back up. It’s a really critical period. Each store is different, clearly in Houston, there was flooding but once sorted, you still had population, you still had people. In the Sandy situation, you had entire areas where people could no longer live. You had relocation, I think that would be similar to Katrina. The recovery curve, I think, is going to vary depending on what happened on the people front.

I think Irma, similarly, it had an impact, but people are back. Maria, on the other hand, people couldn’t really … it was so devastated that it’d be really hard for a business owner to do business if the people you’re serving don’t have a place to live and don’t have some kind of stability. I think it does vary. Just to give you an example of what that economic responder can look like, this is a program that when Irma hit, we reached out to some partners and said, “Listen, we know we have 90 days. Could you help us support to create an emergency relief program for Irma-affected businesses?” We launched it on September 15, we will be doing this, as I said, over a three month period. In one of our first clients, they got served, they were in the Keys, which I think if you read, it got really impacted.

It’s called Cocos Boat Rentals, and the owner, his name is Jason, came down from Minnesota and did a lot of boating trips to Florida before deciding to skip the cold winters and created this boat rental business. I think things were going well until Irma hit and knocked the Keys. When they got back, he noticed it didn’t just affect business, but all his customers. Nobody was renting boats, people were asking how he’s doing but he estimated that just in the time that Irma came and left the Keys, and through early September when we were there, so about a week, in that month he estimates that 48% of his business was lost, and $25,000 to $30,000 worth of equipment. They had to do their own cleanup, they only had one employee but even that employee couldn’t come back because they had no home.

They recovered by helping accommodate that individual in their home to work forward. He was in a situation where he needed money for pretty much everything, because the income had completely stop.

Gene: Did he have insurance or anything? If you’re running a boating business down in the Keys, there is a risk of something like this disaster happening more so than if you’re running a boating business in Minnesota on a lake. You know?

Paul: Absolutely. Here’s now where timing plays a role. Insurances, even FIMA, all these resources are available, but the time it takes to make those resources available can be long enough where the window for you to stay up and running, and or be shut down, could come and go.

Gene: I always wondered that, about businesses. When they’re getting relief from FIMA or even collecting insurance money, you’re absolutely right. I mean, come on, you’re dealing with the government, right? It can’t happen overnight, and I wonder, sometimes I think geez, how do these businesses survive the period between the disaster and when they actually get funding from some of these organizations? I guess you see that as well.

Paul: That’s exactly why I said it’s a short window. Just to share some statistics, and these are coming from a research foundation that looked at something like 200,000 small business customers, the average business in the United States, so they didn’t look at the Amazon’s, but the mom and pops. The average transaction volume that goes into their bank statements is about $400 a day. The average business in this country only has about 26 days of actual cash reserves. What happens is, if and then we’ll talk about ways to mitigate, but when you’re living or dying on $400 a day, a disruption like that can literally put you in the negative. The timing sensitivity of responding is key. When Sandy happened, if you read the example, it took a year for the federal government to approve funds.

By that time, of course, businesses were either shuttered, or they had the insurances and they were able to weather the storm. We are talking about a situation in this country right now where the vulnerability is extremely high, cash volatility in this country, even to the person, is extremely high. Every little thing that disrupts the norm is going to teeter you into a risk of shutting down. That’s why I said we look at ourselves as economic first responders, because if we don’t inject capital, and it’s not a lot of money, but it’s a precious amount of money at the right time.

Gene: Let me get back to the boating business then. You guys were able to help them out. First of all, I’m curious to know, how did they even find you? How did they know that you existed and you got connected to them? Once you did get connected to them, what did you do to help them?

Paul: They way we, of course, we don’t market ourselves directly to consumers, because we don’t have that kind of budget. We had always networked ourselves to different business partners. First and foremost, our bank partners. A lot of people go to the banks and to the, for example, when the SBA sets up a relief effort, they work through what they call Small Business Development Centers. These are federally-funded centers that provide technical assistance, business advice. What happens is, in these centers, we, our people have connected with specific individuals in those areas so that they know who we are, they know what we do, and we let them know that we relay the capital for this kind of response. When word got out, which in these kinds of situations, any help is communicated very quickly, we found them through those connections. They would go to the local SBDC, for example, or local bank. They would be talking about their needs and someone would say, “You should talk to Accion.”

Gene: Got it.

Paul: Once you reach us, we work with you one on one, as we talked about earlier, our turnaround time averages about 12 days from the time you start to the time you finish. This program, because of the need, it’s even more accelerated. In a matter of days, you get funded by Accion and that’s kind of the response that people need, because until the insurances come, until the FIMA funds come, until all those other resources can really make their way, you need to make it to that first critical period. That’s what we do.

Gene: If I was a business, it’s kind of a risk business to finance, right? They just lost half their business in the storm, I’m sure banks aren’t lining up to lend them money. What did you ask of them? Did they have to provide collateral, or was this a completely un-collateral … Any personal guarantees? What can a business owner expect if they’re going to get that kind of financing from you?

Paul: Basically the thing about us is we were already designed to meet the needs and as I said earlier, for people that were credit-challenged, meaning we’d lend to people that have credit scores that the banks won’t accept. We lend to people that don’t really have collateral, because if they did, often times what would they need the loan for?

Gene: In other words, you’re crazy.

Paul: Because we’ve learned over 25 years how to manage that risk to a tolerable level. That’s what we do. I say we’re like the Star Trek Enterprise, we boldly lend where no bank will go, but we know how to manage the risks. What we do look at is we have to look and understand that you have the ability to repay the loan. That means that we look at your holistic business and personal picture, because we also take a Hippocratic oath. We don’t want to provide money if it’s only going to indebt you. We want to provide money that we know you can repay, because we report to the credit bureau so that we can build your personal credit. We want to make sure that the far majority of the people that we serve are building positive credit history. It’s all about cash flow for us.

In this case, while his business stopped, he would have been able to evidence that he had a business. He would have been able to evidence that with enough time, he could get back to a certain level. We knew we had enough visibility on that kind of activity to be able to support him at a given level. Some of this is equipment-related, in a sense, even though we’re not boat sales people, there’s something there that could be considered collateral. How much you can liquidate, I don’t know, but our intent is to essentially follow the business practice that we have now.

Gene: You had mentioned before about the Small Business Development Center, and that’s how you got connected. SBDCs are great, and they are usually connected to universities all around the country. They do provide a lot of resources to business owners, so if I’m a business owner and I’m in an area that’s been affected by some natural disaster and earthquake or a hurricane or whatnot, you certainly as a Small Business Development Center might be the first … I need help, so I could turn to them. Any other resources that would come to mind that you would recommend to me if I was … where would I turn to?

Paul: I think there are a couple things, and now because going places is hard, there are some sites that I think can localize all their resources. One is disasterassistance.gov. What that does is you enter the information for your specific location, and disasterassistance.gov tries to marshal all their resources for your specific geography. I think that’s what’s important. We don’t want to generalize, we want to be really, really customized. That’s one.

The other, of course, is the one time that the SBA actually directly lends is in disasters. Otherwise, they pretty much stand behind the banks or organizations that do the lending, using their guarantee. The one time they actually have to marshal resources, do the direct [decisions], it’s when they have a disaster. I would recommend SBA.gov, and right now you can look /funding-program/disasterassistance. That summarizes by storm, so you have resources for Harvey in the counties that are eligible. You have resources for Irma, and you have the resources for Maria.

That’s, I think, a useful site. Then for not necessarily resources, but preparing for the inevitable next one, there’s a nifty little site I’ll call ready.gov. R-E-A-D-Y.gov.

Elizabeth: We’ll put that in the show notes.

Paul: It educates people on how to prepare for and respond to emergencies. What do you do when you hear there’s a hurricane watch? What do you do 24 hours? How can you prepare? Just personally, right? Your physical safety? Which I think is, it’s critical. I would say those three sites should give more than enough to begin. Then from that, visiting the centers is great, but as much as you can find, if you have power, online those three are probably the most comprehensive and simple enough to get you.

Gene: You were mentioning some of the sites like ready.gov, that would actually help you prepare and ask you these questions. I’m going to kind of turn it back on you, Paul, people listening to this podcast, anywhere you operate a business, you’re prone to some type of natural disaster, whether it’s earthquake or hurricane or tornado. We’re all at that risk. Give me some advice. I run a 10 person company, what should I be doing to prepare my business for a potential disaster? What would you do if you were in my shoes?

Paul: Absolutely. I think the first point is what you just highlighted. We need to expect the unexpected, and to do that, given how hand to mouth all businesses really are, that means you need to build a reserve. There’s probably two ways to do that. You either save … if you only have 26 days reserve on average, and these storms can take a while to recover, how can you grow so that you either have in cash savings for three months, or if you need the cash for the day to day, it’s in the sunny days that you should get some form of line of credit. Some kind of credit, you don’t want to be looking for capital after a storm. You want to be looking for capital now, and I would say size that line of credit equal to three months of operations. What do you need for three months of operations?

Even if you never use that line of credit, that is instant liquidity at a time when everybody else will be applying you could be ready to continue paying your rent or any other near-term needs, because you have the ability to reset. That would be the second thing I would say. Obviously, I think one of the things that comes to light is to mitigate really costly downsides. This is beyond that emergency period insurance, right?

Gene: Right.

Elizabeth: I was hoping you’d say that, Paul.

Gene: For god’s sake, we’re sitting here in a building of, there’s a huge insurance company. Thank you.

Paul: I think people are becoming more educated. I think everybody’s talked about flood insurance, the government behind that. You have business interruption insurance. Clearly, you have property. Those boats should have some kind of insurance on them that in time, you’d be able to recover. There are others, and think being able to speak to a broker about all the right coverages, it can help recoup the physical assets as well as the lost business. Those are really, really critical, but you need that line of credit or savings in that interim so that you can bridge from where you are at today, day one of the disaster, until those 90 days where those insurance proceeds do come in so that you can mitigate and minimize that kind of interruption.

Gene: Makes sense.

Paul: The other practical things, I think we should learn from really devastating situations. One of the things that we took a look at was for Hurricane Maria, FIMA has progress reports in the key signs of recovery. What was interesting for me was what they considered mission critical. I just want to articulate them to the listeners, because there could be practical ways to mitigate each of these. Number one was self service. Day one after Maria, only 5% of the island had communication. What does that tell you as a business owner? Maybe it’s worth getting a shorthand radio or a walkie talkie. It doesn’t cost a lot of money, for $100 you’d be able to communicate with your staff, your team. You’d be able to do something when even the big carriers are down. Potable water, only 44% at the time of the hurricane had it. Water’s obviously something that if you’re a local business, you could do. I think more practically, that line of credit is important because ATM’s shut down.

There were only 114 on the entire island that operated, so even if you have the cash, you can’t get to it and no one’s really keeping them safe at their business. That line of credit, I think, is really critical so that you can avoid the runs at ATM’s that aren’t working anyway. Interestingly, generators. All of this works if you have electricity. I think a few thousand dollars to invest in a generator, even if it doesn’t help you save your inventory, you can work your computer to look at the resources, you can communicate. That could be a cost effective investment in a situation where an entire grid goes down. You at least have the means for some period of time to communicate, because without electricity, you really are back to the dark ages. Then, gas stations. Only 40% were even operating, so having some gas for that generator is a very practical thing that doesn’t cost a lot, would be worth the investment.

When these things strike, if it strikes to the same degree as it happened there, or I guess it was Katrina before that, you have the means in that first week or two to navigate, to reach out, to leverage resources, to communicate, and I think it can help you or at least minimize the pain that that storm is going to bring.

Gene: If worse comes to worst, you can always just borrow some money from Elizabeth. That’s right. She seems to have ready cash.

Paul, this is great stuff. Just some takeaways that I’ve learned from this, obviously a natural disaster can affect anybody, so we all have to be prepared for that. As far as being prepared, we want to know where to go, what our resources are. You’ve given some good websites, Small Business Development Centers, SBA, ready.gov, good place to go to go do some checklist to prepare yourself. I think the best preparation that you can do is to make sure that you’re really flush with your own resources. In other words, save, put money away. Have some cash in the bank, have available line of credit, have necessary equipment that’s used, like a generator, for when a disaster occurs.

You’ve got to be thinking ahead. The biggest issue, this whole conversation comes down to it’s not just you as the business owner who’s saving their business. You have all these people that rely on you for their livelihoods, your employees. Even your own customers, suppliers, vendors. They’re expecting that you’re looking ahead and thinking of these things, because they’re going to be leaning on you pretty heavily if disaster comes. It’s a really, really important topic. Paul, thank you very much. Paul Quintero, CEO of Accion, and Accion, again, huge fan of the company. If you’re out there looking for financing, this is not a traditional bank. This is a non-profit that provides financing and then also-

Elizabeth: Training.

Gene: -helps you spend the money the right way, really.

Elizabeth: Tons of resources.

Gene: A great organization, and Paul, we really appreciate you coming on.

Paul: Thank you very much.

Elizabeth: Alright, that’s going to wrap it up for another episode of the Small Biz Ahead Podcast. We want to thank Paul Quintero for being our guest, and we’ll talk to you in a couple days.